PREV ARTICLE

NEXT ARTICLE

FULL ISSUE

PREV FULL ISSUE

THE HISTORY OF THE GOLD STANDARDThe upcoming Künker Auction features quite a number of great gold coins. This article by Ursula Kampmann lays out the history of the gold standard illustrated with lots in the sale. Some great eye candy here, including some nice U.S. rarities. -Editor The Gold Standard: How and Why Gold Became the Most Important Metal For Coins For centuries, silver was the preferred metal across the world when it came to coins and savings. In the 19th century, that changed. We'll explain how and why, and illustrate what happened with the help of coins that will be coming under the hammer on 30 September and 1 October 2020 in the Künker Auction entitled ‘A Numismatic Gold Treasure'. By Ursula Kampmann on behalf of Künker It actually all started with Sir Isaac Newton, or rather, with the huge gold deposits discovered in Brazil, and the trouble they caused him. These finds pushed down the price of gold in such a way that the established mint ratio between gold and silver coins had to be constantly recalculated. Even Isaac Newton – who was, at the time, master of the Royal mint in the Tower of London – failed to keep up with these developments. In his final adjustment in 1717, he valued the silver coins too highly. This effectively led to them disappearing from circulation.

01 - Great Britain. George III. 1/2 Sovereign 1817, London. Rare in this condition. Nearly FDC. Estimate: 800 euros. From Künker Auction 340 (2020), No. 2777. And so, England switched to the gold standard in practice long before a corresponding law was passed. It wasn't until 1774 that parliament confirmed gold coins as legal tender. Silver coins only had to be accepted up to the amount of 25 pounds.

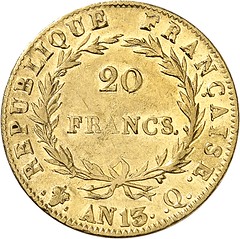

02 - France. Napoleon. 20 francs AN 13 (= 1804/5) Q, Perpignan. Only 522 pieces minted. Nearly extremely fine. Estimate: 2,000 euros. From Künker Auction 340 (2020), No. 3340. England therefore played a rather special role. In most other countries across the world, silver remained the metal of choice for minting coins. France, on the other hand, worked with bimetallism. Napoleon's 1803 monetary law had established the long-standing legal mint ratio of 1 (gold) : 15.5 (silver).

Three Possible Options

03 - Australia. Victoria. Sovereign 1855, Sydney. Very fine to extremely fine. Estimate: 2,000 euros. From Künker Auction 340 (2020), No. 2585.

Price Fluctuations in the Ratio Between Gold and Silver

04 - France. Napoleon III. 100 francs 1862 BB, Strasbourg. Only 3,078 specimens minted. Extremely fine to FDC. Estimate: 1,700 euros. From Künker Auction 340 (2020), No. 3767. This caused problems for every nation whose currency, like France's, was based on a fixed ratio between gold and silver coins. Some clever contemporaries used the exchange rate differences to make a hefty profit. They exported some here and imported some there, successfully lining their own pockets with a handsome profit. The result: at times, France had far too few silver coins, while the United States of America had far too few gold coins. The enormous price fluctuations were therefore a disaster for lawmakers. No sooner had they established the ratio between gold and silver coins than the exchange rate changed and a new law would have to be passed in order to prevent losses for the treasury. And it didn't make matters any easier when, in 1859, a huge deposit of silver ore was discovered in Virginia City. The mines there would yield almost 7 million tonnes of pure silver by the time they closed. As a result, the price of silver also plummeted. In the long term, it fell from 60 p in 1870 to 52 p (1880) to 24 p (1910).

05 - Great Britain. Victoria. Pattern for the Sovereign of 1839, London. Very rare. Extremely fine from Proof. Estimate: 2,000 euros. From Künker Auction 340 (2020), No. 2838. Theory and Practice: Why Did the Gold Standard Prevail? Researchers have established two different theories as to why the global economy ended up committing to the gold standard in the long term. One theory claims that people no longer wanted to live with the constantly fluctuating prices of precious metals. The other theory claims the cause is rooted in nations' efforts to adapt their own monetary system to the nation with which they did most business. Well, at the start of the 19th century, there were two nations vying for economic leadership: Great Britain and France. We know who came out on top. Thanks to industrialisation, London became the most important financial centre in the world. Two thirds of all world trade were financed by the pound sterling. Switching your currency to the gold standard therefore gave you privileged access to this financial centre.

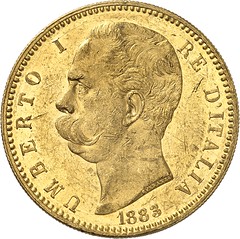

06 - Italy. Umberto I. 100 lira 1883, Rome, in accordance with the specifications of the Latin Monetary Union. Only 4,219 specimens minted. Nearly extremely fine. Estimate: 2,500 euros. From Künker Auction 340 (2020), No. 2852.

France and the Latin Monetary Union

07 - Belgium. Albert I. Pattern of 100 Francs 1911, Brussels, in accordance with the specifications of the Latin Monetary Union. Extremely rare. Extremely fine. Estimate: 50,000 euros. From Künker Auction 339 (2020), No. 2202. Just think about when the Comstock Lode was discovered in Virginia City 1859 and its yield caused the price of silver to collapse. Italy was the first country in the French currency area to adapt to this development. In 1862, it changed the alloy used to make the circular blanks for its low-value coins, decreasing the silver content from 900 to 835 per mille – much to the annoyance of France, where coins were minted with 900 per mille. In other words: the aforementioned clever contemporaries imported French silver coins into Italy, had them smelt down and reminted there into more Italian coins of the same denomination and then reimported them into France to change into other French silver coins and so on. In 1864, France found itself forced to drop the fineness of its coins to 835 per mille. But at that time, Switzerland had already decided to mint silver coins from an alloy of 800 per mille silver. And be sure those oft-mentioned clever contemporaries planned to do what they always did: they made a good profit at the expense of the general public.

08 - France. Napoleon III. 100 francs 1868, Strasbourg, in accordance with the specifications of the Latin Monetary Union. Only 789 specimens minted. Extremely fine to FDC. Estimate: 2,200 euros. From Künker Auction 340 (2020), No. 3779. The Latin Monetary Union of 1865 was actually nothing other than an attempt to make this impossible. Although some representatives at this conference lobbied vehemently for the gold standard, France prevailed with its bimetallic system. However, it failed to push the system through at an international level during the large monetary conference called by France in 1867. At that point, it became clear that there was no future in the bimetallic system.

09 - Albania. Zog I. 100 francs 1926, Rome, in accordance with the specifications of the Latin Monetary Union, without being a member of the Latin Monetary Union. Extremely fine. Estimate: 1,750 euros. From Künker Auction 340 (2020), No. 2521.

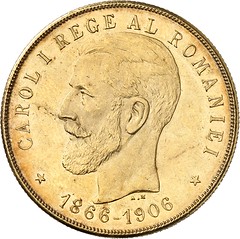

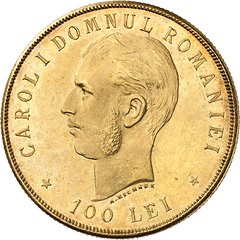

10 - Romania. Carol I. 100 leu. 1906, Brussels, in accordance with the specifications of the Latin Monetary Union, without being a member of the Latin Monetary Union. Only 3,000 specimens minted. Extremely fine to FDC. Estimate: 3,000 euros. From Künker Auction 340 (2020), No. 2983.) Although the wonderfully colourful maps suggest time and again that the world was enthusiastic about the Latin Monetary Union, the fact that individual nations issued coins in the same weight as the golden 20-franc or silver 5-franc pieces did not mean that they wanted to preserve the bimetallic system. They simply wanted to have coins that were compatible with the French coins.

11 - Germany/Hesse. Ernst Ludwig. 20 mark 1905. Extremely fine +. Estimate: 750 euros. From Künker Auction 340 (2020), No. 2705.

Germany Opts For the Gold Standard

This wasn't a particularly big step for these nations; it was hardly noticeable for their citizens. This is because – and this point cannot be stressed enough – the gold standard did not mean that there weren't any silver coins in circulation. It simply meant that all means of payment, i.e. small coins, bank deposits and banknotes, could be converted into gold at any time. By the way, it's a myth that the French coins paid as war reparations in 1871 were reminted into 20-mark pieces. Of the 5 billion marks paid, 4.248 billion came in bills of exchange denominated in English pounds. Germany exchanged these papers in London for the gold it needed to produce its currency. The silver coins, which were withdrawn from circulation and whose raw material was thrown back onto the market, caused the price of silver to fall even further.

12 - USA. 5 dollars 1847, Charlotte. Very rare. Very fine +. Estimate: 8,000 euros. From Künker Auction 340 (2020), No. 3033.

Silver Producers in the USA

13 - USA. 20 dollars 1859, New Orleans. One of the best preserved specimens. NGC AU58. Estimate: 25,000 euros. From Künker Auction 340 (2020), No. 3229. And then in 1859, as mentioned earlier, the Comstock Lode was discovered. This discovery had an impact on the price of silver. During a crisis that would go down in history as the ‘Long Depression', the government established a series of measures, including the adoption of the gold standard in the Coinage Act of 1873.

14 - USA. 5 dollars 1874, Carson City. Extremely rare in this condition. NGC MS61+. Estimate: 10,000 euros. From Künker Auction 340 (2020), No. 3073. It was only three years later that there was any serious resistance. The Coinage Act became the ‘Crime of ‘73'. The silver producers developed a superb public relations strategy that concealed their own interests to such an extent that, to this day, you will read occasionally in books about American history that it wasn't their own overproduction that caused the price of silver to fall, but rather the sale of silver in Germany following the currency changeover. In fact, in 1878, the Bland-Allison Act was passed, over the veto of President Hayes, which forced the treasury to purchase a certain amount of silver every year and use it to mint silver coins. As this silver was bought at the market price, this development was less about returning to a bimetallic system and more about support buying in favour of the country's own silver producers.

15 - USA. 10 dollars 1878, Carson City. Only 3,244 specimens minted. NGC AU50. Estimate: 3,000 euros. From Künker Auction 340 (2020), No. 3206. In the same year, the United States of America organised an international monetary conference, where they, as one of the biggest producers of silver in the world, attempted to convince other countries to switch to a bimetallic monetary system so that they could sell their own silver around the globe. The conference failed. Germany didn't even send a representative, while the British delegates were ordered to block all proposals. The ever-growing gap between supply and demand remained a problem. In 1890, the American Congress passed the Sherman Silver Purchase Act, which replaced the Bland Allison Act and meant that the federal government became the second-biggest buyer of silver in the world. By the way, the biggest buyer was the British government in India, which was attempting to hold up the rapidly falling price of silver and therefore support the Indian rupee.

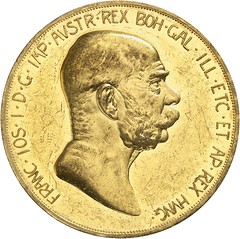

16 - Austria. Franz Josef I. 100 krone 1908, Vienna. NGC PF60. Estimate: 2,500 euros. From Künker Auction 340 (2020), No. 2922.

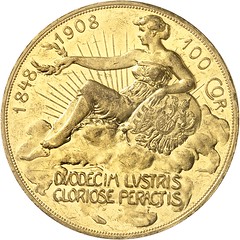

17 - Hungary. Franz Josef I. 100 krone 1907, Kremnica. Extremely fine +. Estimate: 2,500 euros. From Künker Auction 340 (2020), No. 3018.

18 - Russia. Alexander III. 10 ruble 1894, St. Petersburg. Only 1,007 specimens minted. Nearly extremely fine. Estimate: 2,000 euros. From Künker Auction 340 (2020), No. 3007. In this one year, 1890, the price fell from 1.16 dollars per ounce to 0.69 dollars. On 1 November 1895, the treasury temporarily stopped issuing silver dollars. And it wasn't alone: over the course of the 1890s, Russia, Japan and the Habsburg Monarchy also switched over from their bimetallic systems to the gold standard. France and with it the countries of the Latin Monetary Union – with the exception of Italy – had already done this in 1878.

Commercial Interests Versus Agricultural Society

Never before in history had society been monetised to this extent. In Great Britain, the amount of money in circulation increased from 255.4 million pounds in 1850 to 11,303.6 million pounds in 1913. The proportion of coins – as opposed to bank notes and bank deposits – fell from 23.9% to 12%. A similar pattern can be observed in Germany, where 1.38 billion mark in 1875 increased to 18.31 billion mark in 1913, while the proportion of coins fell from 42.4% to 18.3%. This monetisation went hand in hand with the transition of the economy from self-sufficiency to a society based on the division of labour. Those who worked in the city depended on their savings retaining value and preferred stable gold, while the farmers, with their ever-increasing mortgages, relied on inflation to help them pay off their loans. The almost worldwide transition to the gold standard is a sign that the most important segments of a country's population were no longer based in its rural areas, but in its cities.

At no point did the gold standard mean that all coins of a certain country had to be made from gold. It merely comprises:

And this is what caused the gold standard to fail in the long term. No country in the world had the discipline to issue only as much paper money as its gold reserves allowed, even in political emergencies. And in Europe, this meant that the system collapsed at the beginning of the First World War. The high demand for physical gold among citizens could no longer be met by the countries' gold reserves. Although many countries returned to the gold standard after the end of First World War, this collective realisation that only physical gold can be relied upon to retain its worth means that gold coins are still the first choice when it comes to safely storing assets during a crisis. The Künker Auction entitled ‘A Numismatic Gold Treasure' will be a brilliant opportunity to combine collecting with investing in gold.

To visit the Künker website, see:

Wayne Homren, Editor The Numismatic Bibliomania Society is a non-profit organization promoting numismatic literature. See our web site at coinbooks.org. To submit items for publication in The E-Sylum, write to the Editor at this address: whomren@gmail.com To subscribe go to: https://my.binhost.com/lists/listinfo/esylum All Rights Reserved. NBS Home Page Contact the NBS webmaster

|